Home Prices Are Growing 3X Faster Than Incomes - The Math That Broke America

When homes cost 5.7x annual income rather than 3x, homeownership doesn't just get harder. It becomes mathematically impossible for most Americans.

The Ratio That Reveals Everything

There's one number that explains the entire housing crisis better than any other:

The price-to-income ratio.

For decades, the rule of thumb was simple:

Homes should cost about 2.5 to 3 times your annual household income.

Earn $80K? You could afford a $240K home.

Earn $100K? You could afford a $300K home.

The math worked. Families could save for a down payment, qualify for a mortgage, and build wealth through homeownership.

Then everything broke.

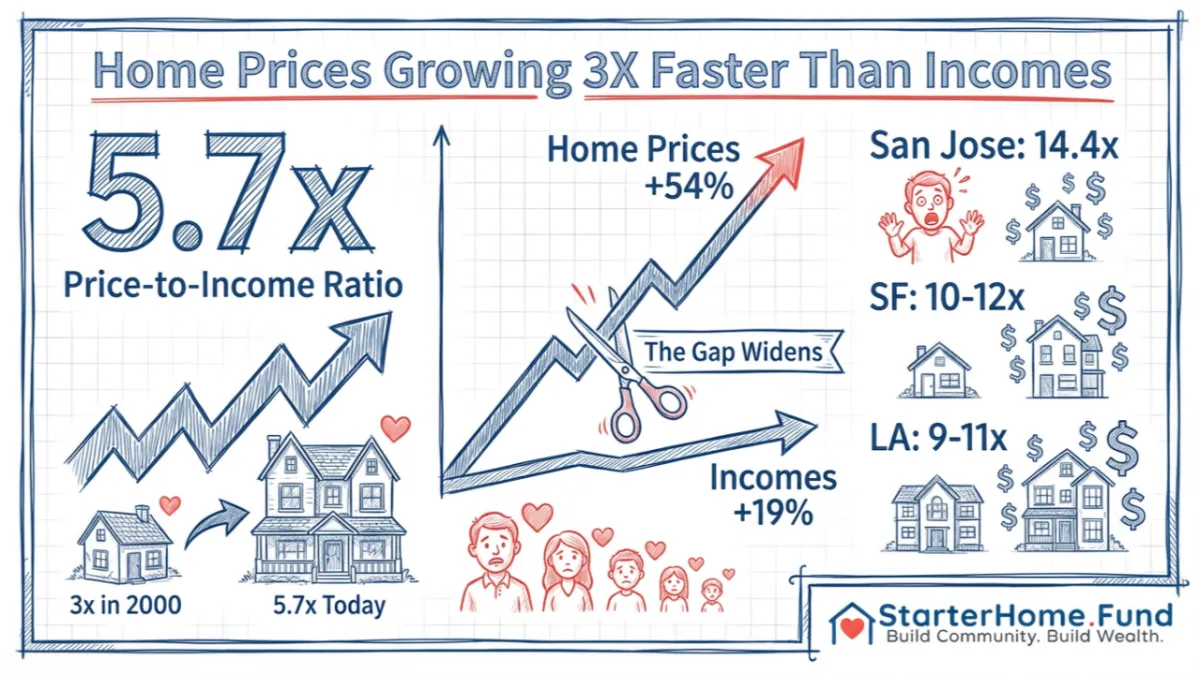

The New Normal: 5.7x and Rising

Today's national median price-to-income ratio sits around 5.7x.

That's not a temporary spike. That's not a market anomaly. That's the structural reality of American housing. And in expensive markets? The ratios are apocalyptic:

Markets with price-to-income ratios over 8x:

San Jose, CA: Homes cost 12-14x annual income

San Francisco, CA: 10-12x

Los Angeles, CA: 9-11x

San Diego, CA: 8-10x

Honolulu, HI: 9-11x

At a 3x ratio, homeownership is attainable.

At a 5x ratio, it's challenging.

At a 10x ratio, it's mathematically impossible for median earners.

What Happened?

Two forces collided:

1. Home prices skyrocketed

Median home price 2013: ~$270K

Median home price 2025: ~$415K

Increase: +54%

2. Incomes barely moved

Median household income 2013: ~$63K

Median household income 2025: ~$75K

Increase: +19%

When home prices grow 3x faster than incomes, the affordability gap doesn't just widen—it becomes permanent.

The Markets Where the Math Died

Let's look at real numbers from some of the most distorted markets:

San Jose, CA:

Median home price: $2,020,000

Median household income: ~$140,000

Price-to-income ratio: 14.4x

To afford the median home in San Jose using traditional lending ratios, you need an income of $595,389.

The median household earns $140K.

That's a $455,000 income gap.

It's not an affordability challenge. It's a complete market failure.

Naples, FL:

Median home price: $865,000

Required income: $264,020

Actual median income: ~$75,000

Gap: $189,000

Seattle, WA:

Median home price: $875,000

Required income: $231,475

Actual median income: ~$105,000

Gap: $126,000

These aren't markets functioning poorly. These are markets that stopped functioning for median earners.

Why This Matters for Investors

When price-to-income ratios break, three things happen:

1. Homeownership rates collapse: We've already seen this. First-time homebuyers have been priced out. The average first-time homeowner is now 40 years old.

2. Rental demand explodes: People who can't buy are forced to become lifelong renters. This creates sustained upward pressure on rents — and opportunities for multifamily investors — but permanently locks out homeownership for about 37% of the US population (100 million people locked into the Renter class, in perpetuity).

3. Alternative models become viable: When traditional homeownership is mathematically impossible, people will embrace alternatives: Condo conversions, Resident Owned Communities, manufactured housing, shared equity models, and community land trusts.

This is where the opportunity lives.

The Properties Nobody Wants

While everyone chases luxury (Class A) apartment developments in hot markets, there's another story playing out:

Affordable multifamily properties are failing.

Why?

Because they can't raise rents fast enough to cover rising expenses.

Because Nonprofit owners can't refinance at higher rates.

Because they've been neglected for years and now face massive deferred maintenance.

These properties hit the market at $20K - $100K per door in markets where new construction costs $200K - $400K+ per door. (Like Portland and Seattle)

Everyone sees distressed assets.

We see arbitrage opportunities with a mission.

Our Solution:

Acquire distressed, affordable properties at steep discounts (Usually 40% of ARV)

Stabilize through condo conversion and mission-aligned capital (Investors like you) 😍 🏦

Maintain affordability while delivering institutional returns

Exit at $175-$300/door

→ → Our model brings the price-to-income ratios into a 2.5x ratio. Because we help low- to moderate-income families with about $90,000 in household income, we can easily help them buy a new home for $225,000. ← ←

All of a sudden... the math works again. This is what we call Compassionate Capitalism. 😍 🏦

The Trend Isn't Reversing

Some people think this is cyclical. That prices will "come back down" and ratios will normalize.

They won't.

Here's why:

Supply constraints: Zoning, NIMBYism, and construction costs keep new supply limited

Demand drivers: Millennials and Gen Z are in peak household formation years

Institutional capital: Private equity and REITs now compete with individual buyers

Interest rates: Even if rates drop, prices will rise to absorb the savings

The price-to-income ratio isn't going back to 3x in our lifetimes. It's structural.

And that means the affordable housing crisis is permanent—unless someone builds a different model.

The Bottom Line

StarterHome.Fund has fixed the Price-to-Income Ratio. We provide homes that low-to-moderate families can easily afford. ($90K income = $225K home = 2.5 Price-to-Income Ratio)

But people still need housing. They still want stability. They still want to build wealth.

The investor who provides that—while preserving affordability—wins.

Starterhome.Fund is solving the housing affordability crisis and the down payment dilemma for 10,000 families.

And we're delivering 18% AAR to investors who join us.

👉 Invest in the housing model that actually works for median earners. Join Our Investor Club - 18% AAR →

Data Source: Harvard Joint Center for Housing Studies, State of the Nation's Housing 2025