Kelly Fest

Mortgage Loan Officer

Grow Your Empire

With a dual background in real estate and mortgage finance spanning over two decades, I provide a comprehensive lens on asset acquisition and capital structure.

Now representing NEXA Mortgage, I leverage our lean brokerage model to bypass the high overhead costs of traditional banking.

This allows us to deliver superior pricing and highly engineered lending solutions that align with your long-term fiscal objectives.

Investment Loan Programs

Your situation is one-of-a-kind—

I’ll help you find the perfect funding for your next deal.

Asset-Focused Funding for Modern Empires. We look at gross potential income from the property, not your W2s.

Zero Income Proof, Infinite Scaling Potential. Your personal debt-to-income ratio stays out of the equation entirely.

Scale Past the 10-Loan Ceiling. Traditional limits don't apply here; build a portfolio as large as your ambition.

The Shortest Path from LOI to Keys. Experience the speed of a loan process that values your time as much as your equity.

No Tax Returns, Just Real Estate Results. Qualify based on the property’s potential, not your historical IRS filings.

Versatile Funding for Any Portfolio Structure. From single-family residences (SFR) to multi-unit assets or even portfolio-wide blanket loans—we can fund your specific strategy.

Financing Built for Leverage. Harness the strength of the deal to fund other investment opportunities.

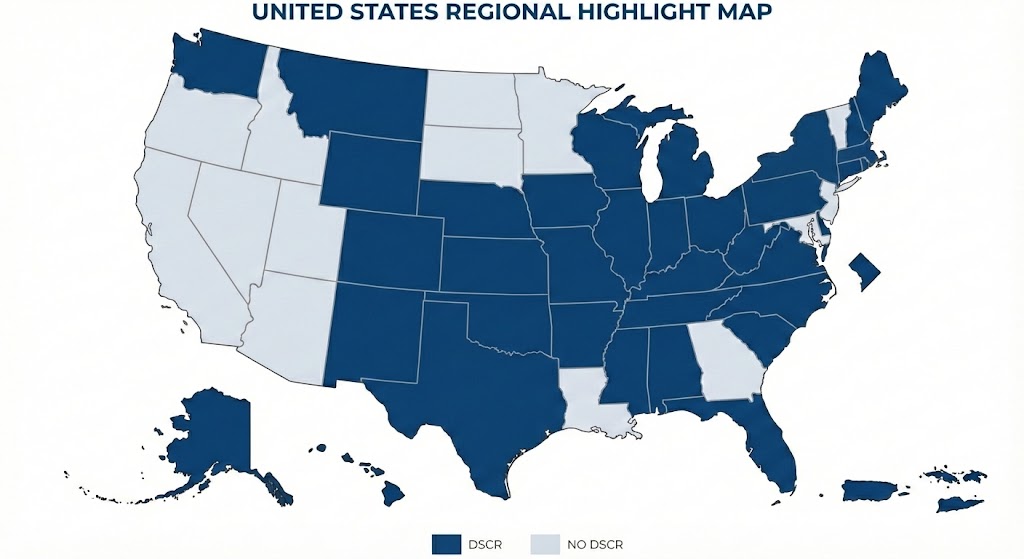

Where Can We Do DSCR's?

Wondering how to get a real estate investment loan, step by step?

What documents do I need?

DSCR Loans Only Need the Following

Entity documents

- Articles of Incorporation/Organization

- Operating or Partnership Agreement

- EIN letter from IRS

- Certificate of Good Standing

Schedule of REO

2 months bank statements - show downpayment and any reserves

Copy of lease & rent rolls (if vacant, use market rents)

Property Documents:

- Purchase Contract (if a purchase)

- Operating Statements (last 24 months)

- Environmental Report (if applicable)

- Property Condition Report (if required)

- Survey

Personal & Business Financial Statements

Including YTD Profit & Loss Statement and Balance Sheet

Business Bank Statements

2 most recent consecutive bank statements for all accounts. If you are doing a Bank Statement Loan, then we need most recent 12 or 24 months of Business Bank Statements and Personal Bank Statements.

Personal & Business Tax Returns

2 to 3 years for each guarantor plus 2 to 3 years for the entity, all schedules

Entity Documents

Articles of Incorporation/Organization

Operating or Partnership Agreement

EIN letter from IRS

Certificate of Good Standing

Schedule of Real Estate Owned

All real estate owned by the entity and guarantors, showing address, rental income, & mortgage balance

Property Documents

Purchase Contract

Rent Rolls

Operating Statements (last 24 months)

Environmental Report

Property Condition Report (if required)

Survey

SBA Loans Need the Following

Detailed summary of the loan request

3 years business tax returns

Year-to-Date P&L and balance sheet

3 years personal tax returns

Borrower information/Resume

Personal financial statement

Business debt schedule

Credit authorization completed & signed for soft pull

Last 2 months of business bank statements

Address of the property

Is the business owned 100% by a U.S. Citizen(s) or ITIN holders?

***Great for owner occupied properties like doctors or small businesses

Foreign Nationals & Foreign Investors

If no ITIN, then we need passport from your home country and documentation of your current address, such as a utility bill or lease agreement. We can do DSCR loans (both purchase and refinance) for Foreign Nationals living in the U.S. and Foreign Investors who live abroad.

If you're selling one property and buying another, don't forget your 1031 Exchange!

Our Calculator Lab includes 21 different real estate investing calculators

We Offer Short Term Rental Financing Using AirDNA Data

Learn More

Podcasts for Investors

20 Frequently Asked Questions

1. What is a "No-Ratio" DSCR loan?

A no-ratio loan is a specialized product where the lender does not require the rental income to exceed the mortgage payment (a DSCR of less than 1.0). This is ideal for properties undergoing a "turnaround" or short-term rentals that have high potential but low current documented income. The formula is DSCR = Net Operating Income (NOI) / Total Debt Service (PITIA)

2. Can I qualify for a DSCR loan as a first-time real estate investor?

Yes! Many first-time investors believe they need a long history of property management to qualify for specialized financing, but that isn't the case. At NEXA Mortgage, we offer DSCR (Debt Service Coverage Ratio) programs that focus on the cash flow of the property rather than your personal employment history or years of experience. As long as the rental income covers the mortgage payment (PITIA), you can secure financing for your very first investment.

3. What is the benefit of a DSCR loan over a traditional mortgage?

The primary benefit is flexibility. Unlike traditional loans, DSCR loans do not require tax returns, W-2s, or debt-to-income (DTI) calculations. This is a game-changer for self-employed investors or those looking to scale their portfolios quickly. Since the loan is based on the property's performance, it allows you to grow without being limited by your personal income.

4. Do you provide commercial real estate financing nationwide?

Absolutely. Whether you are looking at a multifamily complex in Texas, a retail space in Florida, or a short-term rental in Tennessee, we provide nationwide financing solutions. Our team understands the nuances of different markets across the U.S., ensuring you get the best commercial terms regardless of where your target property is located.

***Offering DSCR & commercial loans in only these states or territories currently: AL, AK, AR, CO, CT, DE, FL, HI, IL, IN, IA, KS, KY, ME, MI, MS, MO, MT, NE, NH, NM, NC, OK, OH, PA, SC, RI, TX, TN, VA, WA, WV, WI, WY, District of Columbia, Puerto Rico, US Virgin Islands

5. Can I close a loan in the name of an LLC?

Yes, and we often recommend it. Most commercial and DSCR loan programs allow—and sometimes require—you to close in the name of an LLC or business entity. This provides an added layer of liability protection for you as an investor. If you are a first-time investor and haven't set up an entity yet, we can guide you through how this impacts your loan application.

6. What are the typical down payment requirements for investment properties?

For most DSCR and commercial investment loans, you can expect a down payment ranging from 15% to 25%. While this is higher than a primary residence, the trade-off is a much faster closing time and fewer "hoops" to jump through regarding your personal finances. We also offer "no-ratio" options for properties with unique potential that may not yet be fully occupied.

7. Can I use a DSCR loan for a Short-Term Rental (Airbnb/VRBO)?

Absolutely. DSCR loans are perfect for vacation rentals. We can often use data from platforms like AirDNA or the property’s actual rental history to project income, allowing you to qualify even if the property is currently vacant.

8. What is a Prepayment Penalty on a DSCR loan?

Most DSCR loans come with a prepayment penalty (often a 3-2-1 or 5-4-3-2-1 structure). This means if you refinance or sell within the first few years, you pay a small percentage. However, we offer "buy-down" options to reduce or eliminate these penalties if you plan to flip or refi quickly.

9. How many DSCR loans can one investor have?

Unlike conventional loans, which usually cap you at 10 properties, there is often no limit to the number of DSCR loans you can hold. This makes them the primary tool for investors looking to scale a massive nationwide portfolio.

10. Does a DSCR loan show up on my personal credit report?

Since these are "business-purpose" loans closed in an LLC, they typically do not report to your personal credit bureaus. This keeps your Debt-to-Income (DTI) ratio low for other personal purchases like a primary residence or a new car.

11. What qualifies as a "Commercial" residential property?

In the lending world, any residential building with 5 or more units is considered commercial. These properties are valued based on their Net Operating Income (NOI) rather than comparable sales, which is where specialized commercial financing becomes necessary.

12. Can I get a loan for a Mixed-Use property?

Yes. If your property has a retail storefront on the bottom and apartments on top, it qualifies for mixed-use financing. We look at the combined income of both the commercial and residential units to determine the loan amount.

13. What is the minimum credit score for a commercial investment loan?

While requirements vary, most competitive commercial programs look for a score of 660 or higher. However, if the property's cash flow is exceptionally strong, there are often workarounds for lower credit scores. We do have a few DSCR programs for borrowers with a credit score as low as a 600, but these deals include an increase in points and closing costs.

14. Can I refinance a commercial property to pull cash out?

Yes. Cash-out refinances are a popular way to "recycle" equity. You can use the cash from one property’s appreciation to fund the down payment on your next nationwide investment. In some instances, you can also use cash out for reserves.

15. Do I need to provide a Personal Guarantee (PG)?

Most DSCR and commercial loans are "recourse," meaning a personal guarantee is required. However, for larger commercial deals or specific portfolios, we can explore non-recourse options where the lender’s only collateral is the property itself.

16. What are "Reserves" and why do I need them?

Lenders want to see that you have "liquid" cash left over after closing (usually 3–6 months of mortgage payments). This ensures you can handle a vacancy or a repair without defaulting on the loan.

17. What is the "BRRRR Method" and can these loans help?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. Our DSCR loans are the "Refinance" engine of this strategy. Once you’ve renovated a property and placed a tenant, we use a DSCR loan to pay off your hard money and pull your initial capital back out.

18. What is an "Interest-Only" option?

To maximize monthly cash flow, many investors choose an Interest-Only (IO) period for the first 10 years of the loan. This lowers your monthly payment significantly, though you won't be paying down the principal balance during that time.

19. Can I use a 1031 Exchange with your commercial loan products?

Yes. We frequently work with 1031 Exchange accommodators. This allows you to sell a property and "roll" the capital gains into a new investment property through our DSCR or commercial programs without paying immediate taxes. This is a primary strategy for nationwide investors looking to "level up" their portfolios. The only caveat is that some DSCR programs do not allow you to use subordinate financing when a 1031 exchange is involved, so be sure to ask.

20. Can I use "Gift Funds" for my down payment on an investment property?

Yes, we have specific programs that allow for gift funds. While it is true that most traditional DSCR and commercial lenders strictly require the down payment to be the investor’s own seasoned funds, we offer flexible solutions for those receiving assistance from family or business partners. Whether you are using gift funds, "gap funding," or capital from a joint venture partner, we can help you structure the deal to meet lender requirements. We will review your specific asset structure and the source of your funds to ensure you qualify for the best possible rate.

Wealth Preservation Analysis

The Cost of Waiting

Waiting for lower interest rates often leads to higher purchase prices. See how much equity you lose by delaying your purchase.

Current Market

Wait Scenario

Financial Impact

Total Equity Lost

$0

Price increases due to appreciation

Equity you would have owned today

Principal paydown missed while waiting

Monthly Payment (P&I)

*Interest rates vary daily. This tool is for illustrative purposes. Contact Kelly Fest to lock in your strategy today.

Contact Us

Kelly Fest

NMLS # 202374

972-854-3270

NEXA Mortgage LLC

https://nexamortgage.com

NMLS #1660690

AZMB #0944059

Corporate Office

5559 S Sossaman Rd

Bldg # 1 Ste # 101

Mesa, AZ 85212