Blogs

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Do Federal Workers Pay Into Social Security Explained

Do federal workers pay into Social Security? The short answer is: most do, but not all. It really all comes down to when you were hired and which federal retirement system you're a part of.

The Simple Answer to a Complex Question

If you're a federal employee, your connection to Social Security is determined by one of two systems: the Federal Employees Retirement System (FERS) or the older Civil Service Retirement System (CSRS). Think of them as two different roads to retirement, each with its own map and rules of the road.

Your path was essentially chosen for you based on your hire date. A major overhaul back in 1984 changed everything, requiring almost all new federal hires to pay into Social Security just like their private-sector counterparts. This created the FERS system, which now covers over 95% of the federal workforce—that’s more than 2.1 million active employees today. You can find more details on the taxable wage base and its impact on Social Security contributions to see how this works year to year.

FERS vs CSRS Social Security Contributions at a Glance

So, what's the big difference between these two systems? It boils down to one thing: integration with Social Security. The FERS plan was designed from the ground up to work with Social Security, while CSRS was built to be a standalone pension.

This table provides a quick side-by-side comparison.

| Feature | FERS Employees (Hired after 1983) | CSRS Employees (Hired before 1984) |

|---|---|---|

| Social Security Taxes | Yes. Pay standard FICA taxes (6.2%) on earnings up to the annual limit. | Generally no. Do not pay FICA taxes on federal earnings. |

| Retirement Structure | A "three-legged stool": 1. FERS Basic Benefit (pension) 2. Social Security 3. Thrift Savings Plan (TSP) |

A larger, self-contained CSRS pension. TSP participation is optional. |

| Social Security Benefits | Yes. Eligible for benefits based on their entire work history, including federal service. | No, not based on their CSRS federal service. May qualify from other jobs. |

As you can see, this fundamental divide is the most important thing for any federal employee to grasp when looking at their future income. It’s the difference between planning for two income streams in retirement (FERS + Social Security) or one large one (CSRS).

Understanding which system you belong to isn't just a matter of curiosity—it's the bedrock of your entire retirement strategy. It dictates your contributions, your benefit calculations, and how you should plan for your financial future.

Knowing where you stand is the first, most crucial step. If your federal career started after 1983, you can be almost certain that you're paying into Social Security and will receive benefits. If you're a long-time employee who started before then, your situation is likely very different. The rest of this guide will dig into the details of both paths, helping you confirm your status and plan with confidence.

Understanding the Great Federal Retirement Divide

To really get why some federal employees pay into Social Security and others don’t, we have to jump back in time. The year 1984 was a watershed moment for federal retirement, drawing a line in the sand that still defines the financial future for millions of federal workers today. This isn't just a bit of trivia; it's the bedrock of your entire retirement plan.

Before then, things were simple. There was just one system: the Civil Service Retirement System (CSRS).

Think of CSRS as a self-contained, all-inclusive retirement plan. It was built to be the only retirement income a federal employee needed, offering a robust pension funded by hefty contributions from both the employee and the government. Social Security wasn't even part of the conversation for them.

This worked for a long time. But by the early 80s, lawmakers started getting nervous about the long-term financial health of both CSRS and Social Security. They decided it was time to bring federal workers into the same Social Security system as their private-sector counterparts.

The Birth of the Three-Legged Stool

And so, the Federal Employees Retirement System (FERS) was born, covering everyone hired on or after January 1, 1984. FERS threw out the old all-in-one model. In its place, it introduced a philosophy of shared responsibility, famously known as the "three-legged stool."

Each leg of the stool represents a distinct piece of your future retirement income, all designed to work together:

- The FERS Basic Annuity: This is your pension. It's smaller than the old CSRS pension, but it’s still a reliable, guaranteed income stream for life.

- Social Security: This is the big one. As a FERS employee, you pay Social Security (FICA) taxes just like almost everyone else, and your years of federal service help you earn those benefits.

- The Thrift Savings Plan (TSP): This is your 401(k)-style investment account. To make it a powerful tool, the government gives you a generous 5% match on your contributions, which is basically free money for your retirement.

This new structure completely changed the game. For anyone hired under FERS, the answer to "Do federal workers pay into Social Security?" became a straightforward and absolute "yes."

Why CSRS Stands Apart

So, what about all those folks who were already working for the government before 1984? This is where the confusion often comes from.

Employees covered under the old CSRS system generally do not pay Social Security taxes on their federal wages. Instead, they contribute a higher amount—around 7% of their salary—directly into the CSRS fund to pay for their much larger pension. You can find some fascinating historical data on federal annuitants on the Social Security Administration's website that shows just how many retirees fall into this category.

The core difference is simple: CSRS was designed to replace Social Security for a federal career, while FERS was designed to work with it. This philosophical divide explains every major difference between the two systems, from contribution rates to benefit calculations.

This split has huge ripple effects. A CSRS retiree builds their financial plan around a large government pension, supplemented by whatever they've saved in their TSP. A FERS retiree, however, is juggling three income streams, which makes for a more diversified but also more complex retirement puzzle.

For FERS employees nearing retirement, a key piece of that puzzle is figuring out how to bridge the income gap before they can start collecting Social Security. That’s where benefits like the FERS supplement come in. If this is you, our guide explaining what the FERS supplement is and how it works is a must-read.

Ultimately, knowing which side of that 1984 divide you’re on is the first and most critical step in building a solid retirement strategy. It dictates everything from what’s taken out of your paycheck today to the entire financial framework of your life after you hang up your federal hat.

How to Find Out Which System You’re In

Alright, we’ve covered the difference between FERS and CSRS, but theory only gets you so far. The real question is: which system are you in? It’s time to get a definitive answer.

Fortunately, you don’t have to guess. The federal government keeps meticulous records, and the answer is waiting for you in your official employment documents. Let's dig in and find out exactly where you stand in just a few minutes.

Check Your Standard Form 50

Your most reliable source of truth is the Standard Form 50 (SF-50), also known as the "Notification of Personnel Action." You get a new one every time something changes in your career—a promotion, a step increase, even a job transfer. Think of it as the official receipt for every major event in your federal service.

Pull out your latest SF-50 and look for the "Retirement Plan" box (it’s usually box 30). The code there will tell you everything you need to know.

- FERS: The box will likely say "FERS," or you might see a code like "K" or "L."

- CSRS: You'll probably see the code "CSRS" or the number "1."

- CSRS Offset: This is often indicated by "CSRS and FICA" or a code like "C" or "E."

If you can't find your SF-50, just reach out to your agency's HR or personnel office. They can get you a copy in no time. This document is the final word on your retirement coverage.

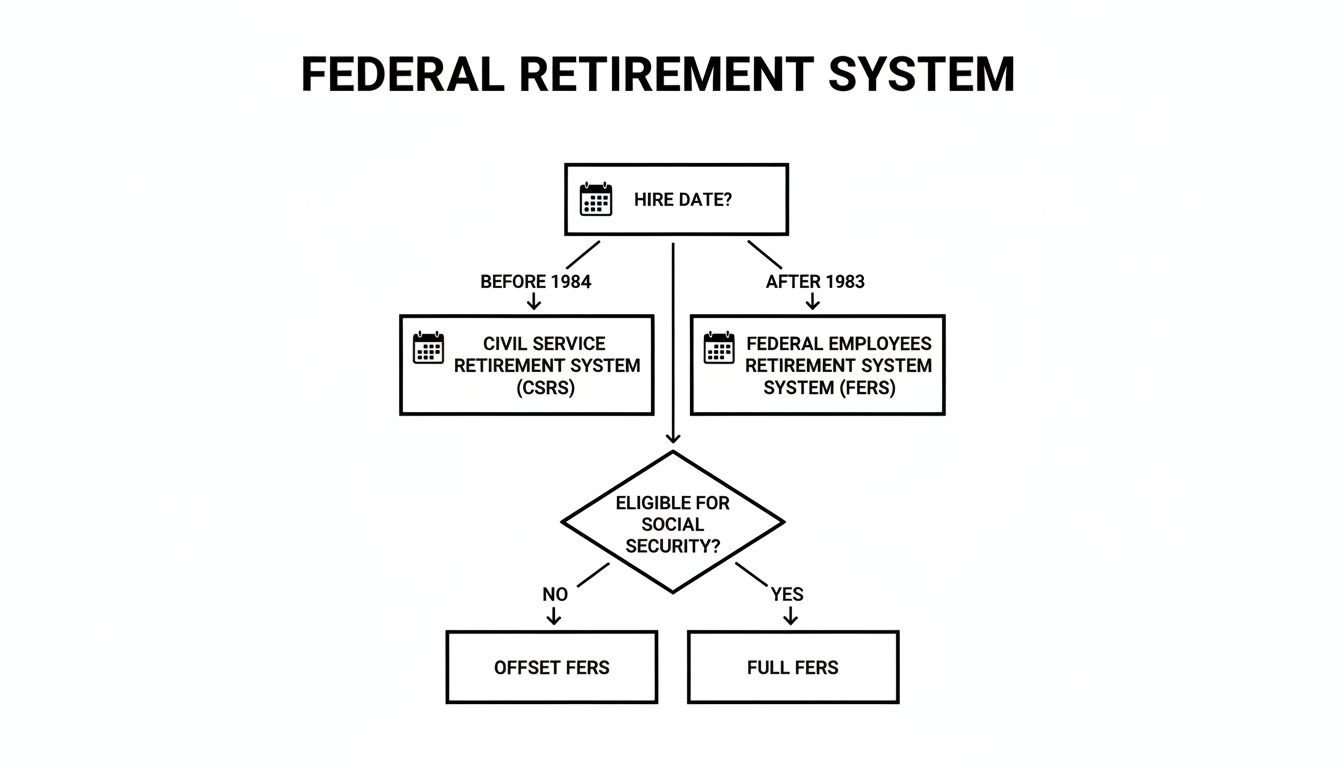

This flowchart helps visualize how your hire date is the key factor in determining which system you were placed in.

As you can see, that January 1, 1984, cut-off date was the great dividing line between the old CSRS system and the modern FERS framework.

Inspect Your Leave and Earnings Statement

Don't have your SF-50 handy? No problem. You can get a quick, real-time answer from your Leave and Earnings Statement (LES)—your federal paystub. The LES breaks down every dollar you earn and every deduction taken out, making it an excellent diagnostic tool.

Scan the deductions section of your most recent LES. You're looking for one specific line item: "OASDI" (which stands for Old-Age, Survivors, and Disability Insurance) or simply "Social Security."

If you see a deduction for OASDI/Social Security, you are paying into the system. It's a dead giveaway that you're covered by either FERS or CSRS Offset.

On the other hand, if that line is missing and you only see a deduction for "Civil Service Retirement" or "CSRS," then you are almost certainly in the classic CSRS system. It's that simple.

Using both your SF-50 and your LES is the best way to get absolute certainty. Once you know your status, you can start planning your financial future with confidence, from calculating your pension to understanding how Social Security fits into your retirement picture.

WEP and GPO: The Two Social Security Rules Every CSRS Employee Must Understand

If you're a federal employee under the older Civil Service Retirement System (CSRS), there are two lesser-known provisions that can take a huge bite out of your retirement income. They’re called the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

Think of them as special rules that adjust Social Security benefits for people who also get a pension from a job—like your federal service—where they didn't pay Social Security taxes. Because CSRS employees don’t contribute to Social Security through their federal job, the government views your hard-earned CSRS pension as a "windfall."

These rules were designed to level the playing field, but for many retirees, they feel more like a penalty. For anyone covered by CSRS, understanding how they work isn't just a good idea; it's absolutely critical to your financial planning.

This isn't just a U.S. issue, either. Public pension complexities are a common challenge in places like the UK, Canada, and EU nations, where civil servants often have their own retirement systems. But in the U.S., where most of the private sector relies on Social Security, the separate system for many federal workers creates this unique and often confusing situation. You can discover more insights on federal worker contributions by digging into the latest official reports from the Social Security Administration.

Understanding the Windfall Elimination Provision (WEP)

First up is the Windfall Elimination Provision, or WEP. This rule can shrink the Social Security retirement or disability benefits that you earned yourself from other jobs. WEP applies if you have a CSRS pension but also worked in the private sector long enough—usually at least 10 years—to qualify for your own Social Security benefit.

Let's say a CSRS employee worked as an engineer for 15 years before starting their federal career, paying Social Security taxes the whole time. When they retire and apply for both their CSRS pension and their Social Security benefits, WEP comes into play. The Social Security Administration will use a different, less generous formula to calculate their benefit simply because they're also getting a CSRS pension.

WEP is not an elimination; it's a reduction. The exact amount of the reduction depends on your years of "substantial earnings" under Social Security, but it can never be more than half of your CSRS pension. Still, it’s a significant cut that can be a nasty surprise if you're not ready for it.

To really get into the weeds on how the numbers work, check out our guide that offers a full explanation of the Windfall Elimination Provision.

How the Government Pension Offset (GPO) Works

While WEP hits your own benefits, the Government Pension Offset (GPO) targets any spousal or survivor benefits you might be eligible for through your spouse's work record. The GPO is much harsher than WEP and, in many cases, will reduce these benefits all the way to zero.

Here's the brutal math: if you receive a CSRS pension, the GPO will cut your Social Security spousal or survivor benefit by two-thirds of your CSRS pension amount. That reduction is often so large that it completely wipes out any benefit you might have otherwise received from your spouse's Social Security.

This isn't just a theoretical problem. Let's walk through a real-world scenario to see the GPO's devastating impact.

Example GPO Calculation

- A retired federal employee gets a $3,000 per month CSRS pension.

- Her spouse passes away, making her eligible for a $2,500 per month Social Security survivor benefit based on his lifetime earnings.

- The GPO calculation kicks in: two-thirds of her $3,000 pension is $2,000.

- Her survivor benefit is then reduced by that amount: $2,500 - $2,000 = $500.

- Instead of receiving the full $2,500 her husband's record provided, she now gets just $500 per month.

As you can see, the GPO can drastically change a surviving spouse's financial outlook overnight. For CSRS employees, this makes planning for a spouse's death a critical, if difficult, conversation. Simply assuming you'll receive a Social Security survivor benefit without accounting for the GPO can lead to a massive income shortfall when you're most vulnerable. Sitting down with a benefits specialist to run these specific calculations is a non-negotiable step in building a truly secure retirement plan.

Building Your Federal Retirement Strategy

Understanding whether you pay into Social Security is far more than a line item on your paystub—it’s the cornerstone of your entire retirement game plan. Which system you fall under, FERS or CSRS, fundamentally shapes the components of your future income and how you should prepare for life after your federal career.

For most feds on the job today, the path is pretty well-defined. The Federal Employees Retirement System (FERS) is intentionally built on a three-pillar foundation. Your success in retirement hinges on getting these three pillars to work together in harmony.

FERS Planning: The Three-Pillar Approach

If you're a FERS employee, your financial future rests on managing three separate income streams. Each plays a different role, and if you neglect one, you could leave a serious gap in your retirement budget.

Think of it like a three-legged stool. It needs all three legs to be stable. Your three pillars are:

- The FERS Basic Annuity: This is your guaranteed pension. It’s not as large as the old CSRS pension, but it provides a steady, predictable income floor you can build the rest of your plan on.

- Social Security: Since you've been paying into the system, your federal service earns you Social Security credits. This piece of the puzzle is a huge advantage because it provides inflation-adjusted payments, making it a powerful shield against the rising cost of living.

- The Thrift Savings Plan (TSP): This is your personal investment account, the government's version of a 401(k). Your own contributions, boosted by the government's generous match of up to 5%, make this your most powerful tool for building real wealth.

A FERS strategy isn't about maximizing just one pillar; it's about orchestrating all three. Your Social Security claiming decision, for example, directly affects how much you might need to pull from your TSP early on. Delaying Social Security could mean leaning on your TSP more heavily at first, but it pays off with a larger, guaranteed income stream for the rest of your life.

For any FERS employee, taking a deep dive into smart Social Security claiming strategies for federal employees is non-negotiable. It’s how you see the full picture of how these three income sources will interact over decades.

CSRS Planning: Maximizing Your Core Benefits

For those under the Civil Service Retirement System (CSRS), the retirement puzzle looks completely different. You generally don't pay into Social Security from your federal job, so your financial plan is much more concentrated and calls for a different set of priorities.

The absolute center of your retirement world is your powerful CSRS pension. This annuity is far more generous than its FERS counterpart precisely because it was designed to be your primary source of retirement income. For a CSRS employee, the name of the game is protecting and maximizing this core benefit.

Key decisions for CSRS employees revolve around this reality:

- Survivor Benefits: Deciding whether to elect a survivor annuity for your spouse is one of the most critical choices you'll make. Yes, it reduces your monthly pension check, but it provides a lifelong income for your surviving partner—a vital safety net, especially since the GPO will likely prevent them from receiving a Social Security survivor benefit based on your work.

- TSP as Your "Gap Filler": Your TSP account is your flexible money. It's the fund you’ll tap for big one-off expenses like a new roof, to cover potential long-term care costs, or simply to supplement your pension for travel and hobbies.

- Healthcare Planning: Without that automatic link to Social Security and Medicare Part A, planning for healthcare takes on an even greater urgency. Your TSP and other personal savings must be ready to step in and cover these potentially significant costs down the road.

While your federal benefits are the foundation, a solid retirement plan also relies on smart financial habits. A practical guide on how to save for retirement can help strengthen your overall financial literacy. No matter which system you're in, a secure future demands a clear-eyed strategy built specifically for your benefits.

Answering Your Top Questions About Federal Retirement and Social Security

Even once you get the hang of FERS and CSRS, some specific questions almost always come up. That’s because everyone’s career path is different, and your time spent working outside the government can throw a few curveballs into the mix.

Let's tackle some of the most common points of confusion head-on. Think of this as a quick-reference guide for those nagging "what if" scenarios.

What Happens If I Worked in the Private Sector Before My Federal Job?

This is a huge piece of the retirement puzzle. If you worked long enough in the private sector to earn your Social Security credits (usually 40 credits, which takes about 10 years), you're on track to receive a Social Security benefit from that work.

But how that benefit interacts with your federal pension is completely different depending on your retirement system.

- If you're under FERS: It’s simple. Your private-sector earnings and your federal earnings both count toward your Social Security benefit. There are no special reductions or complicated formulas to worry about.

- If you're under CSRS: This is where it gets tricky. Your Social Security benefit will almost certainly be hit by the Windfall Elimination Provision (WEP). Because your CSRS pension comes from earnings where you didn't pay Social Security taxes, the WEP rule adjusts the calculation, resulting in a smaller Social Security check.

Do CSRS Employees Still Pay Medicare Taxes?

Yes, absolutely. This is a critical point that trips a lot of people up. CSRS employees don't pay the main Social Security tax (officially known as OASDI), but they have been paying the Medicare portion of the FICA tax since 1983.

This is fantastic news for your retirement planning. It means virtually all federal retirees, regardless of their system, will qualify for premium-free Medicare Part A at age 65. That’s a cornerstone of your healthcare plan in retirement.

Key Takeaway: Don't mix up Social Security and Medicare taxes on your paystub. They're two different things. Even as a CSRS employee, you've been paying into Medicare all along, securing that crucial benefit for yourself.

Can I Switch My Retirement System From CSRS to FERS?

Unfortunately, no. That ship sailed a long time ago. There were specific "open season" periods decades back when CSRS employees had the chance to switch over to FERS, but that window is now permanently closed.

Your retirement system is set in stone based on when you were hired and your service history. The best thing you can do now is understand the system you’re in and plan accordingly.

How Does a Break in Service Impact My Retirement System?

Taking a break from federal service can change everything. If you were a CSRS employee, left the government for more than a year, and then came back after 1983, you were likely placed into a special hybrid system.

This is called CSRS Offset. Under this arrangement, you contribute to both CSRS and Social Security. If you have any gaps in your federal career, it's vital to confirm your exact retirement status to make sure your planning is based on the right rules.

Figuring out these details is the key to a secure retirement, but you don't have to go it alone. Federal Benefits Sherpa provides one-on-one guidance to help you make sense of your unique situation. Schedule a free 15-minute benefits review to make sure your strategy is on the right track.

Dedicated to helping Federal employees nationwide.

“Sherpa” - Someone who guides others through complex challenges, helping them navigate difficult decisions and achieve their goals, much like a trusted advisor in the business world.

Email: [email protected]

Phone: (833) 753-1825

© 2024 Federalbenefitssherpa. All rights reserved