Blogs

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Federal Benefits Open Season: federal benefits open season guide

Every fall, federal employees get a crucial window of opportunity: the federal benefits open season. This is your one big chance each year to take a hard look at your health, dental, and vision insurance and make sure it’s still working for you.

It typically kicks off on the second Monday of November and wraps up on the second Monday of December. During this time, you can enroll in a new plan, switch your current one, or even cancel coverage for the following year.

More Than Just Paperwork: It's Your Annual Financial Check-Up

It's easy to dismiss Open Season as just another administrative task, but I've seen firsthand how treating it that way can be a massive financial blunder. Think of it as an annual check-up for your financial and physical well-being.

So many people just let their benefits roll over year after year. It's called passive enrollment, and it feels easy, but it's often a costly mistake. Premiums change, plan benefits get updated, and your own family's health needs can shift dramatically in just 12 months.

Ignoring this period could mean you're overpaying for coverage you barely use. Or, even worse, you could find yourself underinsured right when a medical emergency hits. With healthcare costs always on the move, last year's best-value plan might be a money pit this year.

To give you a quick overview, here's what the Open Season covers and when it all happens.

Federal Benefits Open Season at a Glance

| Benefit Program | What You Can Do | Typical Timeframe |

|---|---|---|

| Federal Employees Health Benefits (FEHB) | Enroll, change plans or options, change enrollment type (e.g., Self Only to Self Plus One), or cancel enrollment. | Second Monday in November through the second Monday in December. |

| Federal Employees Dental and Vision (FEDVIP) | Enroll, change plans, or cancel enrollment. | Same window as FEHB. |

| Flexible Spending Accounts (FSAFEDS) | Enroll or re-enroll for the upcoming year. Note: FSA elections do not automatically carry over. | Same window as FEHB. |

Changes you make during this period will then take effect on the first day of the first full pay period in the following January.

Your Chance to Optimize and Save

This isn't just about avoiding problems; it's about actively improving your financial situation. The choices you make here directly affect your take-home pay and your family's long-term financial security. You're in the driver's seat.

For example, you could:

- Switch Your Health Plan: Maybe you realize a High Deductible Health Plan (HDHP) with its powerful Health Savings Account (HSA) makes more sense than your current PPO. This one move could lower your monthly premiums and let you build a tax-free medical nest egg.

- Update Dental and Vision: Is your teenager getting braces next year? Now is the time to check your FEDVIP coverage and switch to a plan with better orthodontic benefits.

- Plan with a Flexible Spending Account (FSA): Take a moment to estimate your out-of-pocket medical costs for next year. Funding an FSA lets you pay for those expenses with pre-tax money, which is like getting an instant discount on everything from copays to prescription glasses.

The most expensive mistake I see federal employees make is simply assuming that the benefits they have are still the best ones for them. Taking just an hour or two during Open Season to review everything can literally save you thousands of dollars and give you peace of mind.

Ultimately, taking the time to engage with Open Season is an act of financial self-care. It’s your chance to ensure you aren’t leaving your hard-earned money on the table.

How to Tackle FEHB Plan Changes and Rising Premiums

For most feds, the federal benefits open season really boils down to one thing: the Federal Employee Health Benefits (FEHB) program. This is where you'll make your most significant financial decisions for the coming year, especially with premium costs being what they are today. It’s so easy to fall into the trap of just letting your current plan roll over, but that habit could cost you hundreds, if not thousands, of dollars next year.

Let’s be honest—FEHB premiums have shot up recently. In just two years, federal employees have seen their out-of-pocket premium costs jump by a staggering 25%. That happened with a 13.5% increase one year, followed by another 12.3% hike the next. This makes it absolutely critical to get in there and actively review your options.

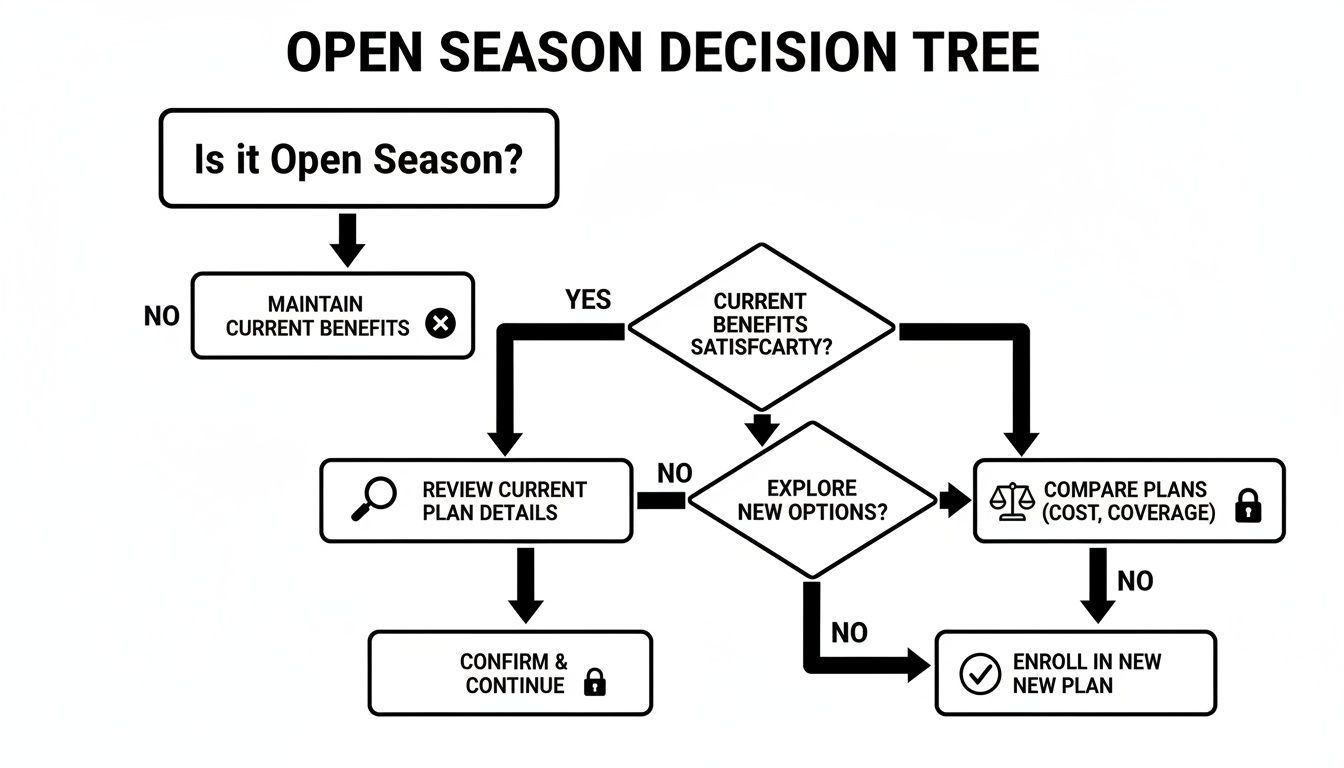

This simple decision tree lays out the basic thought process for reviewing your benefits when Open Season rolls around.

The main takeaway here is that you need a game plan. You have to methodically look at your current coverage, see how it stacks up against other available plans, and then confidently pick the one that truly fits your life.

Look Beyond the Bi-Weekly Premium

When you start comparing FEHB plans, your eyes naturally go to the bi-weekly premium—the number you see vanish from your paycheck every two weeks. While that's an important piece of the puzzle, focusing only on that number is a classic rookie mistake. A plan with a tempting low premium might be hiding a sky-high deductible or an out-of-pocket maximum that could be financially devastating if a real medical emergency hits.

To make a genuinely smart choice, you have to look at the total potential cost. That means getting familiar with a few key moving parts:

- Deductibles: This is what you have to pay yourself before your insurance plan even starts to chip in.

- Copayments and Coinsurance: Think of these as your share of the cost. It might be a flat fee for a service (copay) or a percentage of the bill (coinsurance).

- Out-of-Pocket Maximum: This is your financial safety net. It’s the absolute most you’ll have to pay for covered services in a single year.

- Prescription Drug Coverage: Don't skip this. You need to check the formulary (the list of drugs the plan covers) and the tier system. The cost for the exact same medication can vary wildly from one plan to another.

The goal isn't just to find the cheapest plan. It's to find the plan that gives you the best value for your specific health situation. Sometimes, a slightly higher premium is well worth it if it means a lower deductible and more predictable costs all year long.

A Real-World Plan Comparison

Let's walk through a practical example. Meet Sarah, a federal employee who's pretty healthy but wants to be prepared for anything. She’s trying to decide between two common types of plans.

- Plan A (Traditional PPO): This one has a higher bi-weekly premium of $150, but it comes with a low $500 deductible. Her doctor visits have a predictable $30 copay.

- Plan B (High-Deductible Health Plan with HSA): This plan looks great on paper, with a much lower $80 bi-weekly premium. The catch? It has a $3,000 deductible she has to meet before the plan starts paying for most services.

At first glance, Plan B seems like a no-brainer. The $1,820 in annual premium savings is hard to ignore. But what if Sarah has an unexpected surgery that costs $5,000? With Plan B, she’d be on the hook for the entire $3,000 deductible. On Plan A, she’d only pay her $500 deductible plus any coinsurance.

Of course, the HDHP has a secret weapon: it allows her to contribute to a tax-advantaged Health Savings Account (HSA), which can be used for medical bills or even saved for retirement. To get a better handle on all these nuances, check out our comprehensive guide to the Federal Employees Health Benefits program. Ultimately, the right choice for Sarah comes down to her personal tolerance for risk and what she expects to need from her healthcare in the coming year.

Making Smart Choices Beyond Your Health Insurance

While sorting out your FEHB plan is probably at the top of your list, federal benefits open season is your one big chance each year to adjust other key parts of your financial picture. The right moves here can save you a surprising amount on taxes and give your family better protection. It’s about seeing the whole board, not just one piece.

A common misconception I see is that Open Season is just about health insurance. It's not. This is also your primary window to enroll in hugely valuable tax-saving accounts like a Flexible Spending Account (FSA) or a Health Savings Account (HSA). Think of these as a way to get a discount on all your out-of-pocket medical costs by paying for them with pre-tax money.

Unlocking Tax Savings With an FSA or HSA

So, which one is for you? The choice between an FSA and an HSA really comes down to which health plan you pick. If you’re in a more traditional PPO or HMO, you'll be looking at an FSA. But if you opt for a qualified High-Deductible Health Plan (HDHP), you unlock the incredibly powerful HSA.

One hard-and-fast rule: you cannot have both an HSA and a general-purpose health FSA at the same time.

Making the right choice between an FSA and an HSA is a crucial part of your Open Season strategy. Here's a quick breakdown to help you see the differences at a glance.

FSA vs HSA Key Differences

| Feature | Flexible Spending Account (FSA) | Health Savings Account (HSA) |

|---|---|---|

| Eligibility | Available with most employer health plans (PPO, HMO, etc.) | Requires enrollment in a qualified High-Deductible Health Plan (HDHP) |

| Contribution Source | Employee and/or employer contributions | Employee, employer, or third-party contributions |

| Fund Ownership | Owned by the employer. You lose the funds if you leave the job. | You own the account. It's portable and stays with you if you change jobs. |

| Rollover Rules | "Use-it-or-lose-it." Limited rollover or grace period may apply. | Funds roll over year after year without limit. |

| Tax Advantages | Contributions are pre-tax; withdrawals for qualified expenses are tax-free. | Triple-tax advantage: contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are tax-free. |

| Investment Options | None. It's a spending account, not an investment account. | Funds can be invested in stocks, bonds, and mutual funds, allowing for long-term growth. |

The bottom line? An HSA is a long-term savings and investment tool, while an FSA is a short-term spending account designed for a single year. Both are great ways to save on taxes, but they serve very different purposes.

The biggest mistake I see with FSAs is people overestimating their expenses and losing their hard-earned money. My advice? Pull out last year's records for medical, dental, and vision costs. Then, add in any big-ticket items you know are coming next year—maybe new glasses for the kids or orthodontic work—to land on a realistic contribution.

Smart financial planning also means looking at the bigger picture. When you have a solid handle on your finances, including any debt, you can more confidently decide how much to put into an FSA or HSA. For those looking to get a better grip on their finances, there are many excellent resources on ways to get out of debt.

A Rare Opportunity For FEGLI Changes

Federal Employees' Group Life Insurance (FEGLI) is another benefit to put on your checklist, but your options here are much more constrained. Unlike your health plan, FEGLI doesn’t have a regular "open season" every year.

That said, you can elect or increase your FEGLI coverage in a few specific situations:

- After a Qualifying Life Event (QLE): Major life changes like getting married, divorced, or having a child open a 60-day window for you to make updates.

- During a Rare FEGLI Open Season: These don't happen often. When they do, the Office of Personnel Management (OPM) makes a big announcement.

- By Passing a Physical Exam: You can apply to enroll or increase your coverage outside of these events, but you'll need to provide satisfactory medical information.

This is a perfect time to take a hard look at your current life insurance and ask if it’s still enough for your family's needs. If you want to dig deeper into the nuances, you can learn how to master Open Season for FEGLI in our more detailed guide.

Making Sure Your TSP Aligns With Your Long-Term Goals

Even though the big spotlight during federal benefits open season is always on health insurance, I tell every federal employee I work with that this is the perfect time to give your Thrift Savings Plan (TSP) a thorough check-up. Sure, you can technically change your TSP contributions at any point during the year, but let's be realistic—bundling it with your other big benefit decisions forces you to look at your entire financial picture at once.

This isn't just about stashing money away. It’s about making sure the choices you make today are actually building the retirement you're dreaming of for tomorrow.

The very first question to ask yourself is a simple one: are you contributing at least 5% of your basic pay? If the answer is no, you are literally walking away from free money. That 5% is the magic number to get the full government match. Missing out on that is probably the single most common and costly mistake I see feds make.

Don't Miss These Key Contribution Opportunities

If you're over 50, Open Season is the time to get serious about catch-up contributions. This is a fantastic provision that lets you sock away extra cash above and beyond the normal contribution limits. It's like hitting the accelerator on your savings right when the finish line (retirement) is getting closer.

Think about it this way: a 52-year-old employee who starts making catch-up contributions today could see a massive difference. That extra money, compounded over the final 8-10 years of a career, can easily add up to tens of thousands of extra dollars by the time they retire. It’s a powerful tool, and far too many people leave it on the table.

Your TSP doesn't exist on an island. The choices you make with your FEHB plan, especially in those final five years before you retire, directly determine if you can even keep that health insurance in retirement. A full-picture review is not just smart—it's essential.

How Your Health and Wealth Are Tied Together for Retirement

Here’s a critical detail that trips up a surprising number of federal employees: the unbreakable link between your FEHB and your retirement. To carry your health insurance into retirement, you must have been enrolled in an FEHB plan for the five consecutive years leading right up to your retirement date.

This "five-year rule" gives your Open Season choices some serious long-term weight.

Let's say you're four years from retirement and think about dropping FEHB for a year to save a little cash. That single decision could completely disqualify you from having that vital health coverage for the rest of your life. Aligning your health and savings plans isn't just a nice idea; it's a hard-and-fast rule for a secure life after your federal career.

Finally, take a hard look at how your TSP is invested. Is your risk tolerance what it was a year ago? As you get closer to retirement, or after major life events, you might want to shift your allocation from more aggressive funds (like the C, S, and I Funds) toward the stability of the G Fund. For a deeper dive into this, check out our guide on how to use the TSP for smart federal savings. A quick adjustment now can make sure your investments are still working for your timeline and your goals.

Common Open Season Pitfalls and How to Avoid Them

The biggest mistake you can make during the federal benefits open season is also the most common: doing nothing. It’s easy to let last year’s elections roll over automatically. You're busy, it feels simple, but this passive approach is often a costly financial trap.

You're essentially gambling that nothing has changed—not your family’s health needs, your personal budget, or the fine print of your insurance plan.

But here’s the thing: benefits plans are never static. Every single year, premiums rise, doctor networks shift, and prescription drug formularies get an overhaul. A plan that was a fantastic deal last year could suddenly have a much higher out-of-pocket max or might not cover a critical medication you rely on. That's how you get stuck with unexpected, and often hefty, bills.

Overlooking the Details Can Cost You

Beyond just letting your plans auto-renew, a few other common missteps can really hurt your finances. The good news is that they're all avoidable with a little bit of attention.

One of the most frequent slip-ups I see is miscalculating FSA contributions. Unlike an HSA, a Flexible Spending Account has a strict "use-it-or-lose-it" rule. If you over-fund that account, you're just giving away part of your hard-earned paycheck at the end of the year.

Another classic pitfall is just glossing over your dental and vision (FEDVIP) coverage. It's tempting to assume all plans are created equal, but they vary dramatically, especially for major work like orthodontia or crowns. If you know a big expense is on the horizon for your family, you absolutely have to confirm your plan will actually cover it.

The sheer number of choices can feel overwhelming, I get it. But as benefits specialists always say, taking the time to truly evaluate multiple plans can pay off. Switching to a plan with a different deductible structure could save you hundreds, or even thousands, over the year. You can dig into the specifics with OPM's 2025 Open Season highlights.

Your Quick Reference Checklist

To help you sidestep these common traps, here’s a straightforward checklist. Think of it as the core "do's and don'ts" for a financially smart Open Season.

- DON'T let your plans auto-enroll. DO actively review your current FEHB, FEDVIP, and FSA elections and compare them against what’s new for next year.

- DON'T forget to update your beneficiaries. DO double-check that your designated beneficiaries for life insurance (FEGLI) and your TSP are still correct, especially after big life events like a marriage, divorce, or a new baby.

- DON'T just focus on the premium. DO look at the total potential cost of a health plan—that means factoring in the deductibles, copays, and the out-of-pocket maximum.

- DON'T guess your FSA amount. DO take a few minutes to review last year's medical spending and map out next year's needs. An accurate contribution means you won't forfeit your money.

Ready to Take Control of Your Federal Benefits?

Federal Benefits Open Season is more than just a box to check on your annual to-do list. It’s your single best chance all year to make sure your benefits actually fit your life and your financial goals.

As we've walked through, making smart, deliberate choices about your FEHB, FEDVIP, and FSA can save you a surprising amount of money and, just as importantly, give you peace of mind. Simply letting last year's plans roll over isn't a strategy—it's a gamble. And that’s not a risk worth taking with your family's health or your financial future.

It's easy to feel overwhelmed by the options and just stick with what you know. But getting this right is completely within your reach, especially when you have a clear plan and someone to help you sort through the noise. That's what we're here for.

Your federal benefits are the bedrock of your long-term financial security. The time you invest now to get them right is one of the most impactful things you can do for the person you'll be in retirement.

At Federal Benefits Sherpa, we specialize in bringing clarity to this process. Our goal is simple: to give you the confidence to make the best possible decisions for you and your family. You don’t have to do this alone.

Let us help you get started. We invite you to schedule a complimentary 15-minute benefit review with one of our experts. In a quick chat, we can help you spot potential savings, tackle your most pressing questions, and make sure the choices you make today are building the secure retirement you're working so hard for.

Answering Your Top Open Season Questions

Every year, as Open Season approaches, a few key questions always pop up. Let's tackle them head-on, so you can make your decisions with clarity and confidence.

What Happens If I Just… Do Nothing?

It’s tempting to let the deadline pass, but that can be a costly mistake. If you don't make any changes, your current FEHB and FEDVIP plans will simply roll over into the new year. The problem? Premiums and plan details almost always change, so you could be paying more for less coverage without even realizing it.

Here’s the real kicker, though: your Flexible Spending Account (FSA) contributions will not continue. If you rely on an FSA for healthcare or dependent care costs, you absolutely must re-enroll every single year. Forgetting this step means you lose that benefit entirely.

Can I Change My TSP Contributions During Open Season?

This is a common point of confusion. While you can adjust your Thrift Savings Plan (TSP) contributions anytime you want—not just during Open Season—this period is the perfect trigger to review your strategy.

Think of it as an annual financial check-up. As you're evaluating your health insurance premiums and FSA contributions, it's the ideal moment to see if you can bump up your TSP savings or adjust your fund allocations to stay on track for retirement.

The most critical link to remember is the "five-year rule." You must be enrolled in FEHB for the five consecutive years leading up to retirement to carry that health coverage into your post-federal life. This makes your annual FEHB decision incredibly important as you near retirement.

Is This My Chance to Enroll in FEGLI?

Unfortunately, no. The Federal Employees' Group Life Insurance (FEGLI) program has its own set of rules and does not participate in the annual Open Season.

Opportunities to enroll in or increase your FEGLI coverage are very rare. They typically only happen after a specific qualifying life event (like getting married or having a baby) or during an occasional, OPM-announced FEGLI open season, which doesn't happen every year. Don't put off reviewing your life insurance needs thinking you can just handle it during the fall benefits season.

Feeling unsure about which choices are right for you? The experts at Federal Benefits Sherpa are here to help. Schedule your free 15-minute benefit review to get personalized guidance and ensure you’re making the most of your benefits package.

Dedicated to helping Federal employees nationwide.

“Sherpa” - Someone who guides others through complex challenges, helping them navigate difficult decisions and achieve their goals, much like a trusted advisor in the business world.

Email: [email protected]

Phone: (833) 753-1825

© 2024 Federalbenefitssherpa. All rights reserved