Blogs

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Thrift Savings Plan Vesting: thrift savings plan vesting for FERS and CSRS

When you hear the term "TSP vesting," you might think it's some complicated financial jargon. But the concept is actually pretty straightforward: it's the process of earning full ownership of the retirement money the government contributes to your account.

While every dollar you put in is always 100% yours, the government's contributions have some strings attached. You need to stick around for a certain amount of time before you can walk away with all of it.

What Is TSP Vesting and Why It Matters to You

Think of your Thrift Savings Plan (TSP) as having two main pots of money. The first pot is filled with your own contributions, deducted straight from your paycheck. That money is yours, period. It’s vested from the moment it hits your account.

The second pot is where the government adds its contributions. This is where TSP vesting becomes crucial. Vesting is essentially the government's way of rewarding you for your service. To earn the right to keep some of this "free money," you have to work for a specific amount of time.

Knowing the rules is a big deal for your financial future. If you leave federal service before you're fully vested, you'll have to forfeit the government's automatic contributions plus any earnings they generated. That could be thousands of dollars left on the table.

Your Contributions vs. Agency Contributions

Let's break down exactly what money is in your TSP, because the vesting rules treat each source differently.

Here's a quick look at the different types of contributions and who they belong to.

Your TSP Contributions At a Glance

| Contribution Source | Who Contributes | When It Becomes Yours |

|---|---|---|

| Employee Contributions | You | Immediately |

| Agency Matching | Your Agency | Immediately |

| Agency Automatic (1%) | Your Agency | After a waiting period |

As you can see, most of the money in your account is yours right away. Let's look closer.

- Your Employee Contributions: Every penny you contribute from your salary to your Traditional or Roth TSP is yours from day one. No waiting period, no questions asked.

- Agency Matching Contributions: When you contribute at least 5% of your pay, the government matches it with another 4%. This matching portion is also yours immediately. You've earned it by contributing yourself. You can learn more about maximizing your government matching TSP contributions in our guide.

- Agency Automatic (1%) Contributions: This is the key one. FERS employees get an automatic 1% contribution from their agency, even if they contribute nothing. This is the part that is subject to a vesting period.

The bottom line is simple: The money you put in and the money the agency matches are yours to keep. It's the automatic 1% contribution that you have to work a little longer to earn full ownership of.

Why Vesting Is a Core Retirement Concept

Vesting isn't a concept unique to the TSP. It’s a standard practice in the private sector for plans like 401(k)s. The goal is always the same: to encourage employees to stick around.

By requiring a service period to earn full ownership of employer contributions, companies and the government incentivize loyalty. It helps reduce turnover and the costs associated with hiring and training new people. For you, understanding vesting is the first step to making sure you walk away with every dollar you're entitled to.

How the FERS Vesting Timelines Actually Work

If you're a federal employee under FERS, your TSP vesting isn't a single, straightforward clock. Think of it as two different timers running at the same time for the money the government puts in your account. Getting a handle on how each one works is the key to knowing exactly what money is yours and when.

One pile of government money is yours to keep instantly. The other requires you to stick around for a while before it officially belongs to you. This is, without a doubt, the most important part of the thrift savings plan vesting rules you need to understand.

The Two Timers for Government Money

The government contributes to your FERS TSP account in two distinct ways: Agency Matching Contributions and the Agency Automatic (1%) Contribution. Each has its own vesting rule.

Agency Matching Contributions: This is the easy one. This money is 100% yours from day one. When you put your own money into the TSP, the government matches it. Because you triggered this match with your own savings, it's considered immediately vested.

Agency Automatic (1%) Contributions: This is the portion with the waiting period. Your agency deposits an amount equal to 1% of your basic pay into your TSP automatically, even if you don’t contribute a single dime yourself. This is the money that's subject to a vesting requirement.

Key Takeaway: Here’s a simple way to remember it: The money the government gives you as a reward for your own saving (the match) is yours right away. The money the government gives you just for showing up (the automatic 1%) requires you to prove you’re committed by staying for a few years.

This system is designed to immediately encourage new employees to save for retirement while also giving them a strong incentive to build a career in federal service. For a deeper dive into federal benefits, organizations like the National Active and Retired Federal Employees Association (NARFE) provide a wealth of information.

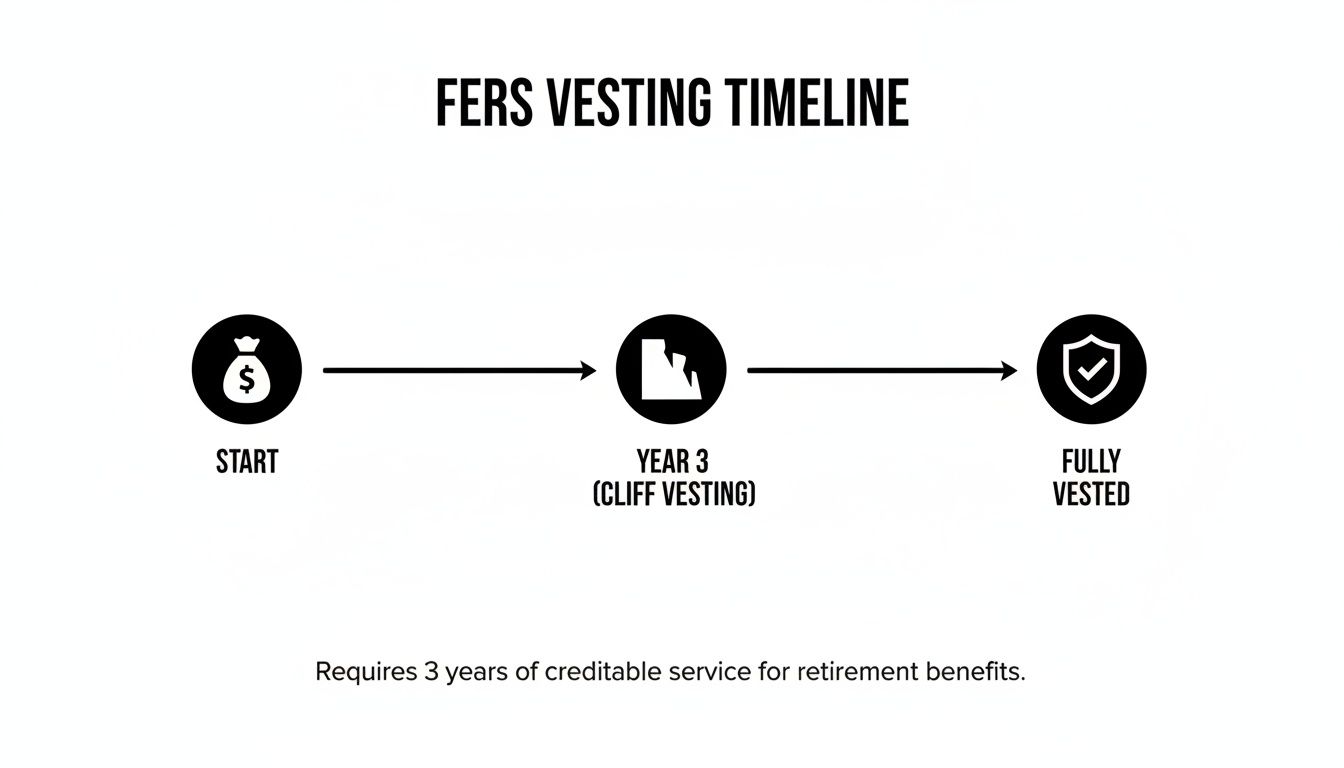

The 3-Year Cliff Vesting Rule Explained

Those Agency Automatic (1%) Contributions are on what’s called a 3-year "cliff vesting" schedule. The term might sound a little dramatic, but the concept is pretty simple. For your first three years of service, you have exactly 0% ownership of this money.

Then, on the day you hit your three-year service anniversary, your ownership goes from 0% to 100% in an instant—like jumping off a cliff. It isn't a gradual increase. If you separate from federal service even one day shy of that three-year mark, you walk away from all of the Agency Automatic (1%) contributions and, just as importantly, any earnings that money has generated.

This is a make-or-break deadline for anyone thinking about leaving their federal job. A simple miscalculation of your service time could mean leaving thousands of dollars on the table.

To make this crystal clear, let's break down how the government's contributions vest.

FERS Government Contribution Vesting Rules

This table shows a direct comparison of the vesting schedules for the different types of money the government puts in your TSP.

| Government Contribution Type | Vesting Requirement | Illustrative Scenario |

|---|---|---|

| Agency Automatic (1%) | 3 Years of Service ("Cliff" Vesting) | If you leave after 2 years and 11 months, you forfeit this entire amount. |

| Agency Matching | Immediate (0 Years) | If you leave after just 6 months, you keep all matching funds you received. |

As you can see, the difference is night and day. One is tied directly to your service time, while the other is tied to your own savings habits.

What Counts as Creditable Service for Vesting?

To track that 3-year timeline accurately, you have to know what the government considers "creditable civilian service." It’s not always as simple as just looking at your start date.

In most cases, creditable service for TSP vesting includes your time in federal civilian employment under FERS. The official start of this clock is usually your Service Computation Date (SCD), which you can find on your SF-50 (Notification of Personnel Action) form.

However, some types of service don't count toward this specific clock. For instance, making a deposit to get credit for active-duty military service is a great move for your FERS annuity calculation, but that time does not count toward your TSP vesting period. The vesting clock is strictly for your civilian service time. It's crucial to confirm your SCD and understand exactly which periods of your work history apply to avoid making a costly assumption about your vesting date.

What Happens to Your TSP When You Leave Federal Service

Thinking about leaving your federal job? Whether you're heading to the private sector or just taking a break, one of the biggest questions on your mind is probably, "What about my TSP?" This is where thrift savings plan vesting becomes incredibly important, as it determines exactly how much of that account balance you actually get to take with you.

It's crucial to understand what happens if you leave before hitting that magic three-year service mark. The money you put in and any matching funds from your agency are yours, no matter what. But those Agency Automatic (1%) Contributions? That's a different story entirely.

Forfeiting Non-Vested Funds on Separation

If you separate from federal service before you have three years of creditable civilian service under your belt, you’ll have to say goodbye to every penny of the Agency Automatic (1%) Contributions you've received. You'll also lose any earnings that money has made. The government takes that money back; it doesn't get shared with your colleagues.

This is the harsh reality of the 3-year cliff vesting rule. Your account balance can literally shrink overnight. For some, this can mean a loss of thousands of dollars, which is why knowing your precise service computation date is so critical before making any career moves.

This timeline really drives home how that 3-year cliff works for FERS employees.

As you can see, your ownership of the Agency Automatic (1%) contributions goes from 0% to 100% the very day you hit your three-year anniversary.

The Break in Service Rule and Reclaiming Funds

So, what happens if you leave and then decide to come back? Good news—a "break in service" doesn't mean those forfeited funds are gone forever. The federal system is set up to let you combine different periods of civilian service to meet that vesting requirement.

When you return to federal service, your previous time counts. Once your combined service adds up to three years, you're officially vested. At that point, not only are you vested for all future contributions, but the TSP will also restore the forfeited amount from your earlier job, including all the earnings it would have made.

Important Note: There's a catch. For this to work, you must have left your own TSP contributions in the account when you separated. If you cashed out or rolled over your balance, you can't get those previously forfeited funds back when you're rehired.

When federal employees leave service, understanding how their TSP funds are handled is crucial. This includes knowing that, like many other retirement accounts, the Thrift Savings Plan is often treated as a type of non-probate assets for estate planning purposes.

A Practical Example of Combining Service

Let's walk through a quick scenario to see how this plays out in the real world.

- Scenario: Maria starts her federal career and works for two years. She then leaves for a job in the private sector.

- Outcome: Since she didn't meet the 3-year rule, Maria forfeits the Agency Automatic (1%) Contributions from those two years.

- The Return: A few years later, Maria comes back to work for a different federal agency. Her two years of prior service are still on the books.

- Vesting Day: After working for just one more year, her total service time hits three years (2 previous + 1 new).

- Restoration: The moment she hits that mark, she becomes 100% vested. The TSP then puts all the agency contributions and earnings she previously forfeited right back into her account.

This rule is a fantastic safety net for anyone who might have an on-again, off-again career in public service. As long as you don't touch your own money in the TSP, you keep the door open to getting back what you earned. And if you are fully vested and considering what to do with your TSP after separating, you can explore your options in our complete guide on how to rollover your TSP to an IRA.

How Vesting Impacts Your TSP Loans and Withdrawals

When it comes to your TSP, your vested balance is more than just a number on your statement—it’s the magic number that determines what you can actually access while you’re still working. Understanding how thrift savings plan vesting impacts your ability to borrow or withdraw is critical for making smart financial moves.

A lot of federal employees are caught off guard when they find out their total account balance isn't what they can actually tap into. The TSP has very clear rules, and they all circle back to one thing: your vested balance.

This means any money in your account that isn’t yet vested—specifically, the Agency Automatic (1%) Contributions before you hit your three-year service mark—is off-limits. Think of it like cash in a time-locked safe that only opens on your vesting anniversary.

The Math Behind Your TSP Loan Eligibility

When you apply for a TSP loan, whether it's for a general purpose or a home purchase, the TSP doesn't look at your total account value. Instead, they calculate your maximum loan amount using the smaller of these two figures:

- 50% of your total vested account balance (or $10,000, whichever is greater).

- A hard cap of $50,000, minus your highest outstanding loan balance from the last 12 months.

The key phrase there is "vested account balance." If you're a FERS employee with less than three years of service, your vested balance will be lower than your statement total because it won't include those unvested 1% agency funds and their earnings.

Let’s see it in action: Imagine a new FERS employee, David, has been on the job for two years. His TSP statement shows a total of $15,000. But $1,500 of that came from his unvested Agency Automatic (1%) Contributions and their earnings. So, his actual vested balance is only $13,500. The maximum he could borrow would be based on that $13,500 figure, not the full $15,000.

Getting this wrong is a common source of frustration. It can be a real shock when the loan amount you qualify for is less than you were expecting. If you want to dive deeper into the loan process, our complete guide on borrowing from your TSP is a great resource.

Hardship Withdrawals and the Vesting Rule

The same rule applies to in-service financial hardship withdrawals. These are meant for employees facing a documented, pressing financial need. Just as with loans, the TSP only lets you pull from your vested balance.

The money that isn't officially yours yet can't be used to cover an emergency. This rule is in place to protect the vesting system, making sure government contributions are only available after you've met the service requirement.

How Vesting Affects Rollovers and Cashing Out

The impact of vesting becomes most obvious when you separate from federal service. At that point, you’ve got decisions to make about your TSP, like rolling it over to an IRA or another employer's 401(k).

When you start a rollover or request a full withdrawal, only your 100% vested balance is yours to take. Any funds that haven't vested are automatically forfeited and go back to the government. This is where leaving before your vesting date really hits home—that non-vested portion of your account simply disappears.

Once your TSP is fully vested and you start planning your next steps, it's a good idea to think about smart retirement withdrawal strategies to make your money last. Understanding vesting is the first step; knowing how to use those funds wisely is the next. Your vested balance is the foundation for your entire financial future.

Common TSP Vesting Mistakes to Avoid

Navigating the rules of your federal benefits can be tricky, and a simple misunderstanding about Thrift Savings Plan vesting can cost you dearly. I’ve seen it happen time and again—federal employees accidentally walk away from thousands of dollars simply because they weren't clear on the vesting timeline.

These aren't obscure, once-in-a-blue-moon scenarios. They are common pitfalls that, with a little know-how, are completely avoidable. Let's break down the most frequent mistakes so you can protect every dollar of your hard-earned retirement savings.

Miscalculating Your Service Requirement

The single most common and painful mistake is getting the three-year service requirement wrong for your Agency Automatic (1%) Contributions. It’s easy to think in round numbers or estimate your anniversary, but the TSP system is black and white. If you leave federal service even one day too early, you forfeit 100% of those 1% contributions and all the earnings they've generated.

Take the classic case of "The Employee Who Left Two Months Too Soon." An employee, we'll call him Alex, was excited about a new private-sector job. He thought his three-year federal anniversary was in May, so he confidently put in his notice for the end of March.

The problem? His official Service Computation Date was actually late May. By leaving just a couple of months shy of his third anniversary, Alex forfeited over $3,000 in agency contributions, plus all the investment growth that money had made for him. Gone.

- How to Avoid This: Never, ever guess your service date. Before you even think about making a career move, pull up your latest SF-50 (Notification of Personnel Action). Find your official Service Computation Date—that is the only date that matters for TSP vesting.

Assuming All Government Money Vests Instantly

Another trap is thinking that all the money the government puts into your TSP is yours right away. While your Agency Matching Contributions are vested from day one (which is great!), the Agency Automatic (1%) Contributions are not. This is a critical distinction that trips up a lot of people.

Newer employees see their TSP balance growing nicely from both types of government contributions and understandably assume it’s all their money. The shock comes later if they decide to leave before hitting that three-year mark, only to discover a chunk of their account balance vanishes.

Think of your TSP account as having different buckets of money, each with its own rule. The cash you put in and the match you earn are yours instantly. The automatic 1% is more like a loyalty bonus you earn by staying for three years.

Ignoring Vesting Before a Career Change

Making a big career decision without checking your vesting status is like playing poker without looking at your cards. Whether you're taking a new job, planning a break from the workforce, or just moving to a different role, your TSP vesting date should be a major checkpoint in your decision-making process.

It’s such a simple thing to verify, but failing to do so is like leaving a bonus check sitting on the table. You earned that money; don't give it back because of a simple oversight.

- How to Avoid This: Add "Check TSP Vesting Date" to the very top of your career-change checklist. Log into your account on the official TSP website or look at a recent statement. Your vested balance is clearly spelled out, showing you exactly what’s yours to keep. This five-minute check provides the clarity you need to make a smart move and protect your financial future.

Common Questions About TSP Vesting

Even after you've got the basics down, a few specific questions about TSP vesting always seem to pop up. Let's tackle some of the most common ones I hear from federal employees to clear up any lingering confusion.

How Can I Check My Vested TSP Balance?

Knowing exactly what’s yours is critical for smart financial planning. Thankfully, the TSP doesn't hide this information.

Just log into your account on the official TSP website. It's right there on your account summary page—you'll see your total balance and, separately, your vested account balance. Your quarterly and annual statements also break it all down for you, showing what's vested and what isn't.

When you're looking at those numbers, just remember the rules of thumb:

- Your Contributions: Everything you've put in, whether Traditional or Roth, is 100% yours from day one.

- Agency Matching: This is also 100% vested the second it lands in your account.

- Agency Automatic (1%): This is the one to watch. It's subject to that 3-year vesting rule if you're a FERS employee.

That "vested balance" line item is the magic number. It tells you exactly what you’d walk away with if you left federal service tomorrow.

Does Military Service Count Toward Civilian Vesting?

This is a fantastic and very common question, especially for veterans who move into a civilian federal job. The short answer is no. Your time on active duty does not count toward the three-year service requirement for vesting in your civilian TSP.

Think of it this way: your civilian TSP vesting clock starts ticking only when your civilian service begins. You can absolutely make a military service deposit to "buy back" that time for your FERS pension calculation, but that's a completely separate process. It has zero effect on your TSP vesting.

Your three-year vesting clock for the TSP is tied to your civilian Service Computation Date (SCD), which you can find on your SF-50 form.

Key Takeaway: Your FERS pension and your TSP have two different clocks. Buying back military time moves the hands on your pension clock, but only civilian service advances your TSP vesting clock.

What Happens to Non-Vested Funds if I Die in Service?

This is where a really important, and frankly compassionate, exception comes into play. If a federal employee passes away while still on the job, the normal vesting rules are set aside.

In the tragic event of an in-service death, the employee’s entire TSP account immediately becomes 100% vested.

That means any of the Agency Automatic (1%) Contributions that hadn't vested yet—plus all their earnings—are instantly considered vested. The full account balance is then paid out to the beneficiaries on file. It's a critical protection that ensures your family receives the full value you've accumulated, no matter how long you've been in the position.

Navigating the details of your federal benefits is the key to a secure retirement. At Federal Benefits Sherpa, we help federal employees make sense of it all and build a plan that works. Schedule your free 15-minute benefits review today to make sure you're on the right track. Visit us at https://www.federalbenefitssherpa.com to learn more.

Dedicated to helping Federal employees nationwide.

“Sherpa” - Someone who guides others through complex challenges, helping them navigate difficult decisions and achieve their goals, much like a trusted advisor in the business world.

Email: [email protected]

Phone: (833) 753-1825

© 2024 Federalbenefitssherpa. All rights reserved